If you utilize the opposite financial to possess a different sort of family purchase otherwise are actually providing the majority of your available money from the closure to pay off another mortgage equilibrium you could find it bundle by far the most tempting.

Reverse home loan Adjustable-prices, otherwise Possession:

- Fee options: Single lump sum payment disbursement, credit line, term, period.

- Interest rate: Yearly changeable which have an effective periodical alter as high as dos% with an existence limit rates of 5% along the begin rates.

Essentially, interest rates was some below having repaired-rates mortgages however, provide better liberty with percentage arrangements such as for example since the discover credit line, term and you will period arrangements.

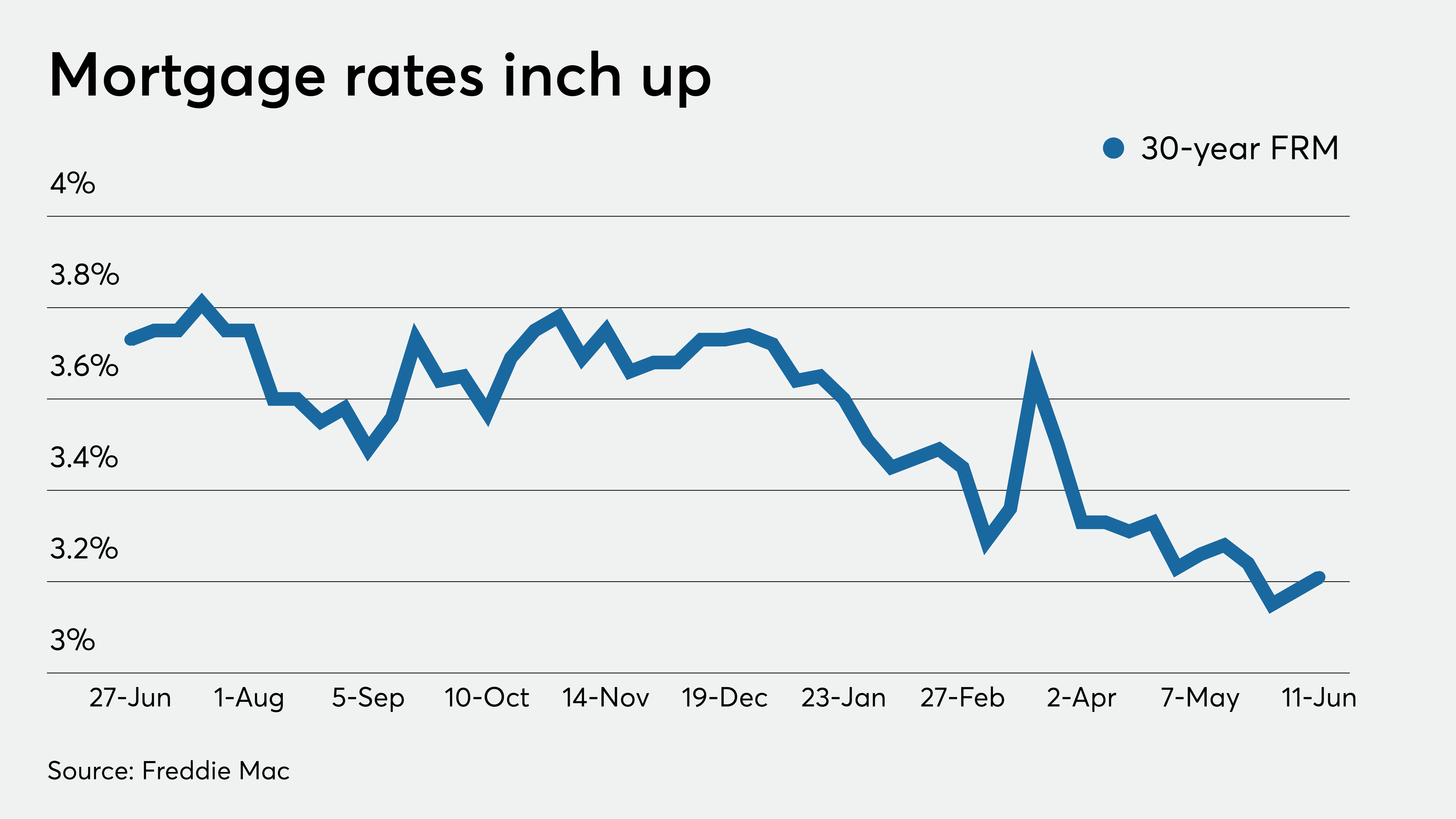

Choosing Fixed-Speed Versus Changeable

You might favor a fixed rates, otherwise a changeable price and you will fixed prices sound great, however they are what’s entitled an effective closed-end appliance and want the borrower when planning on taking the whole loan at very beginning of your purchase. Having individuals that are paying off a preexisting financial and want all their funds to pay off the current mortgage, this might be no problem.

For a borrower who’s no most recent lien on their possessions or a very small you to definitely, this should mean that they would be required to do the entire qualified home loan count at the time the mortgage finance. This could promote a debtor $2 hundred,000, $three hundred,100 or higher within the cash regarding the very first day one they don’t you desire during the time as well as on which they try accruing desire.

This can have a detrimental impact on specific elderly people with needs-founded apps. (Medicaid: Elderly people on the Medicaid and lots of most other need-built applications manage feeling their qualifications insurance firms the brand new abrupt addition of liquid assets) A borrower who’s thinking of only using a fraction of their cash monthly shouldn’t have to shell out interest to the whole count on the very start, deteriorating the new collateral unnecessarily punctual.

A variable speed have a tendency to accrue attention in the a reduced speed during the the current cost however, features an excellent 5% lifetime cover and certainly will wade higher in the event the pricing still rise .

Variable Cost Offer Greater Independency

The newest variable-speed apps perform allow you more independence in the way you could located your own loans. This is simply not https://paydayloancolorado.net/southern-ute/ advised for the variable tool given that a money lump sum payment request might be with the fixed interest levels, but it’s available.

Next option would be a credit line. The HECM credit line is not the just like the fresh Home security Lines of credit otherwise (HELOC) lines of credit that exist at the local bank. The reverse Home loan credit line money develop according to research by the unused part of their line and those fund can’t be suspended otherwise paid down arbitrarily since banking companies normally, and also have complete, recently to the HELOCs.

Consequently the latest personal line of credit develops in accordance with the rate of interest placed on the fresh empty percentage of the line. In other words, using one to exact same $one hundred,one hundred thousand line we’d a lot more than, for those who utilized $45,000 to settle an existing lien as well as your closing will set you back, you might has actually $55,100 left on your own line. So long as you probably did maybe not make use of these funds your line would develop of the same rate as your appeal also your own MIP revival price into the loan.

In case the interest rate are currently 5% plus MIP renewal is .5%, their range perform expand during the 5.5%. That could be around $step three,025 in the first year (having compounding it will be highest). The credit range progress isnt notice individuals try investing your. Its a credit line improve while you never make use of the currency, you don’t accumulated one appeal owing into the growth.